Winning in the Coming B2B Payments Revolution: How Financial Institutions Can Avoid Disintermediation

The SMB B2B Payments market is heating up as the digital revolution continues to ripple through the Financial Services marketplace. The B2B payments market for the Small and Midsize Business segment (up to $1B in revenue) is expected to grow to $9.06 Tr by 2020 – a CAGR of 4.2% from its 2014 base of $7.07Tr.

Despite the rapid increase in consumer payment options and adoption over the last several years, the SMB B2B payments market has been relatively slow to adopt new technologies, instead continuing to rely on checks and ACH payments as their primary payment mechanisms. Overall, 50% of companies still use check and regular ACH as their most common forms of making and receiving payments, with that number approaching 75% for those small businesses under $20 M in revenue.

However, mounting pressures, including high processing costs, increasing check fraud, and the need for streamlined payables and receivables processes, among others, are motivating SMB’s to finally evaluate alternative payment technologies in a significant way.

SMB firms are responsible for 80% of the labor and processing costs associated with the $2.7 Trillion businesses spend on accounts payable processing globally today. Estimates range from $16 to $22 to manually process a B2B invoice, and B2B payments average 45 days to process. Goldman Sachs estimates that firms can cut this to $6-$7 by automating the accounts payable process.

SMB firms are responsible for 80% of the labor and processing costs associated with the $2.7 Trillion businesses spend on accounts payable processing globally today. Estimates range from $16 to $22 to manually process a B2B invoice, and B2B payments average 45 days to process. Goldman Sachs estimates that firms can cut this to $6-$7 by automating the accounts payable process.

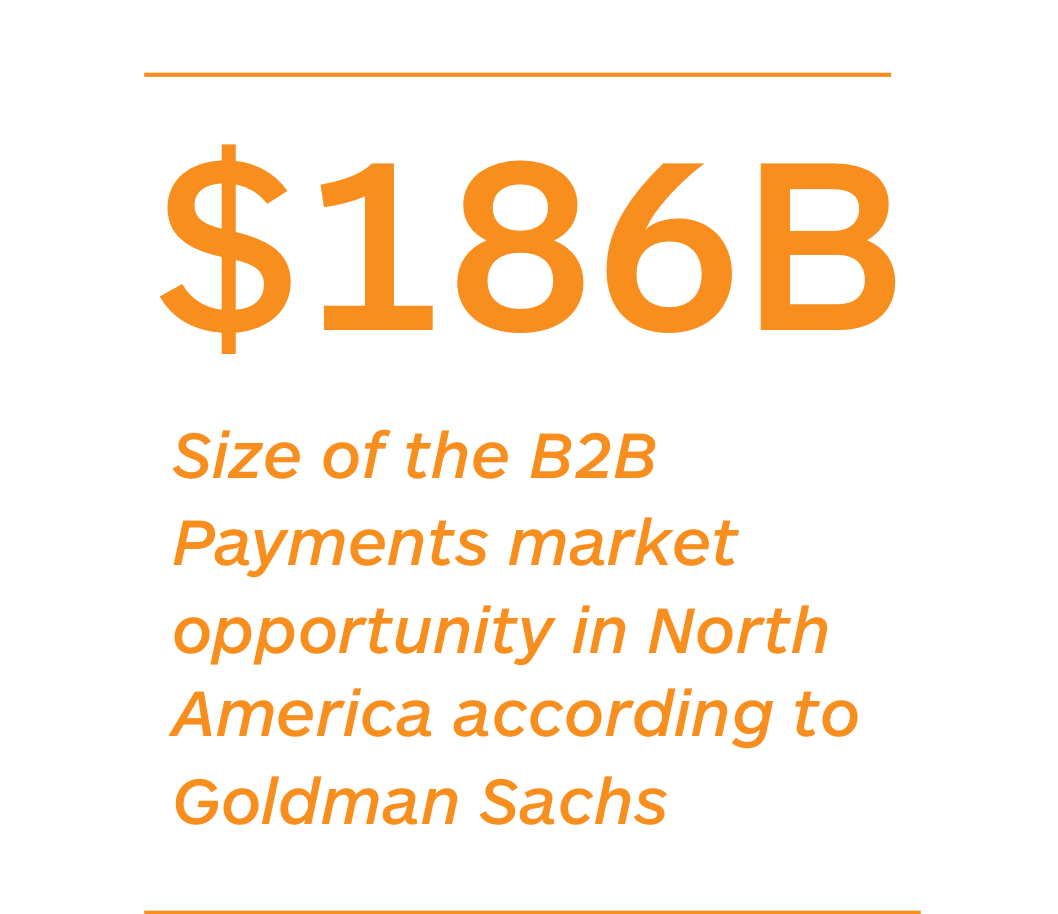

As a result, they value this as a $950B opportunity for payment stocks globally – and a $186B market opportunity in North America!

No surprise then that Mastercard® and PYMNTS.com noted in their Sept. 2018 report “…B2B payments may very well be nearing a tipping point.”

So what is holding firms back from adopting these technologies more quickly when the benefits are clearly so significant? And more importantly, what must financial institutions be doing to prepare for the coming revolution so that they are not disintermediated from supporting their customer’s payment and receivables needs by the plentitude of new electronic payments options that are available today and the innovative new ones that are emerging?

While the answer to the first question varies by firm size, several consistent reasons were noted:

- Payment Acceptance: Will our suppliers accept new payment forms, and how challenging is the on-boarding process?

- Fraud: Concerns about payment fraud, particularly with credit cards and transfers, and increasingly with checks

- Data Security: Is our data secure?

- Integration with Processes: Can the payments solution be implemented within streamlined AP/AR processes?

- Solution Provider: While early adopters are sourcing solutions from FinTechs, many firms prefer to secure these solutions from their trusted bank partners – who are lagging behind on solution development in many instances

We believe another key issue, particularly for SMB’s, is “Payment Solution Overload.” With a rapidly growing solution set based on multiple technologies, SMB’s have a hard time navigating their options and choosing the right solution.

A quick search for Billing and Invoicing Software brings up 388 firms on Capterra, while Payment Processing brings up another 278. In September, Mastercard and Microsoft launched Mastercard Track which provides access to the Global Payments network and a KYC-compliant Track Directory of more than 150 million suppliers globally. CB Insights lists more than 25 Payment Processors and Networks in their FinTech 250 list, with more appearing every day. Real-Time Payments Technology is also quickly gaining traction. Finally, there is an increase in cryptocurrency and blockchain-based global payment systems that is emerging to facilitate the growth in cross-border transactions.

What should traditional FIs do in this market environment to ensure that they remain relevant and the preferred provider for their hard-won Small and Midsize Business customers?

The recently released 2018 FIS Performance Against Customer Expectations (PACE) report provides some insights into this question. They note that “SMB’s are eager for more commercial service, but developing integrated payables/receivables is a low priority for banks. Worse, banks do a poor job communicating about services they already have.”

The good news is that when asked “which types of payment providers they thought would be providing products, services and solutions that help your company improve its payment solutions,” more than 75% of SMB’s expect these solutions to come from banks. This was followed in descending order by Digital giants (Amazon, Microsoft, Google, etc.), Card Network providers, Third-party providers, internally-built solutions and finally a variety of small FinTech providers.

While FI’s appear to be a preferred source for B2B payments solutions, they must continue to innovate, as well as educate, in the face of FI and FinTech competition. The PYMNTS’ 2017 Innovation Readiness Index™ found that 95 percent of surveyed FI’s had focused on innovative payment products in recent years. The PACE report found that “Faster payments/payments infrastructure/payments modernization” was a top 1st or 2nd across all FI types, including Global, Regional and Community Banks as well as Credit Unions.

But clearly, B2B payments product and solution innovation is not sufficient. FI’s must focus on their Go-to-Market strategies in support of this innovation. Their customers are looking to them to be their solution advisors as well as their solution providers in a complex and changing market environment. There is an unmet need for closer alignment and engagement with their SMB clients. This presents both an opportunity for FI’s, as well as a risk.

To maintain their advantage in this environment, FI’s must:

1) Maintain and Demonstrate Thought Leadership

In a complex, changing market environment, FI’s need to demonstrate their understanding of the marketplace and how it is changing. This requires that they regularly gather and package market intelligence on technology, competitors, regulatory requirements, and data security and privacy issues in a rapidly evolving market. They must package and communicate this to their customers – and to their relationship managers and sales teams (see #3 below). This must also inform their product development roadmap and their partnership strategies.

2) Leverage Customer Knowledge and Analytics

FI’s must mine their vast wealth of customer transactional data to identify potential issues and proactively suggest solutions for ongoing business and growth issues such as cash flow predictability and working capital requirements. This extensive customer knowledge is a significant competitive advantage that FI’s enjoy and most FinTech and Third-party providers do not have access to, that many FI’s are not leveraging fully.

Learn more about how one payments processor leveraged customer data to make client-specific solution recommendations. Visit here >

3) Improve Sales Enablement

While FI’s have generally been successful in providing relationship managers to many of their SMB customers to help drive loyalty and satisfaction, these relationship managers must be trained and updated constantly on the dynamic payments marketplace and serve as advisors to their clients if they wish to retain their business. Activating your sales teams and relationship managers with effective guidance via defined integrated customer and seller journeys and standardized best practices playbooks, combined with on-going training, increases the chances of delivering a cohesive customer experience.

Sales need to be updated regularly – we suggest monthly – on trends in the marketplace and the implications for their clients. They need to be provided with the analytical insight at the account-level to proactively engage those customers with solutions that will address their specific needs. They need to be informed about industry vertical-specific solutions so they can understand, anticipate and address client needs as their own.

To learn more about sales enablement best practices, visit here >

While traditional FI’s enjoy a preference today as the primary B2B payments solutions provider, they are at risk of customer defection in a rapidly evolving marketplace that is increasingly focused on payments inefficiencies – and missing their share of this $186B NA opportunity! It will require more than just product innovation to maintain their leadership.

Download the case study on how MarketBridge developed an integrated customer and seller journey best practice playbook for a Fortune 1000 Financial Services provider.